Biden Bucks:

Coming for Your Money (and Your Freedoms)

Dear Reader,

Dear Reader,

The endgame for CBDCs would closely resemble George Orwell’s dystopian 1984. It would be a world of negative interest rates, forced tax collection, government confiscation, account freezes and constant surveillance. I’ll detail what Biden Bucks are, why they threaten your money and liberties and how to escape this digital confiscation of your wealth.

-Jim Rickards

We’ve been following the war on cash for years and advising readers on elite efforts to eliminate cash.

Now these efforts are stepping up and taking on a nefarious tone that also involves surveillance and loss of our freedoms under the guise of central bank digital currencies (CBDCs), or Biden Bucks as we call them.

While the government positions CBDCs as a benefit to consumers in performing transactions, including faster settlements, better security, ease of use and transaction costs that are lower than with cash, it is also crucial to think through the implications of the technology and how it could negatively affect the economy and our individual rights.

On these pages, you’ll learn exactly what Biden Bucks are and why they are not only a threat to your cash but a form of censorship that threatens your freedoms.

Biden Bucks Explained

The U.S. dollar is the largest payment currency and largest reserve currency in the world. So anything affecting the dollar has global implications above and beyond how it impacts U.S. consumers, investors and savers.

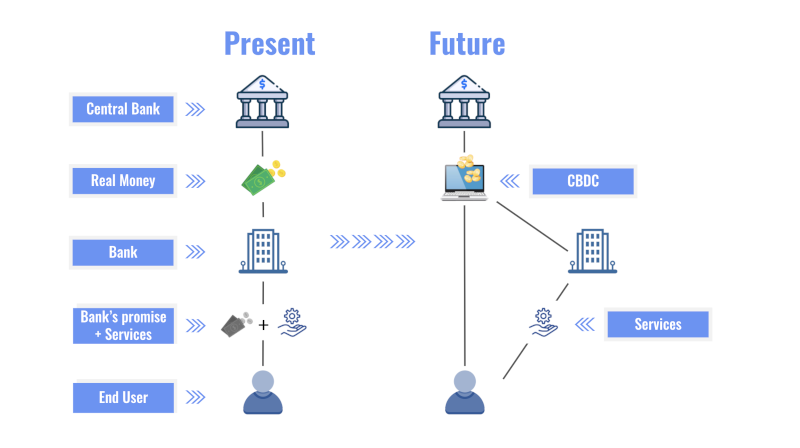

As the name implies, a central bank digital currency is a digital currency. It exists in electronic form. It’s not physical. It’s not something you can put in your wallet or your purse, or carry around, or give to a teller or stick in a parking meter. It’s 100% digital.

The message traffic is encrypted, of course. That’s fairly standard. And central bank in the name just means that these are national currencies created and controlled by central banks. But it’s important to understand they’re not a new currency. They’re a new form of an existing currency, or if you will, they’re a new payment channel.

Digital Currency vs. Cryptocurrencies

CBDCs are digital money, not cryptocurrencies. The differences between CBDCs and crypto are important.

Cryptocurrencies are recorded on a blockchain, which is a particular type of ledger that shows every transaction ever made in each currency. Cryptos also claim to offer anonymity and decentralization, which are said to be virtues but are actually fatal flaws because the “anonymity” is a greater cover for crime and fraud.

I worked with the U.S. Strategic Command to unravel crypto ownership when Isis was using digital tokens to finance its caliphate in 2015–2016. It’s not easy to pierce the veil, but it can be done.

By contrast, CBDCs do not use blockchain; they have a digital ledger accounting system, but it’s not a blockchain. They are the opposite of decentralized; they are highly centralized under the control of a single issuer, usually a central bank.

There is no anonymity. The issuer knows every account holder and every transaction — that’s the whole idea. CBDCs are promoted on the idea that transactions are faster, cheaper and more secure when all money is digital and controlled by a government.

Compared with credit cards, debit cards, wire transfers, Venmo and PayPal, that may be true. Those systems have multiple intermediaries and layers of fees, so CBDCs may actually be able to streamline payments and make the payment system more efficient.

The Advantages of Biden Bucks

The first advantage is it can be faster, cheaper and easier and even more secure than existing payment channels. As I mentioned, it's not a new currency. It's a new payment channel.

So let me just give a simple example.

I go up to any counter, buy a candy bar and I pay for it with a credit card. The retailer that sells it to me takes that credit card receivable and they sell it to something called a merchant acquirer.

A merchant acquirer is a specialized firm, like a financial factoring firm, and they buy up all the receivables from a whole list of merchants, from retailers or whoever is on their list.

They then bundle what could be hundreds of millions of dollars or more of these receivables from retailers. So the retailer gets paid, and the merchant acquirer owns the receivable.

The merchant acquirer then delivers the receivables to the credit card company (Mastercard, Visa, Discover, etc., depending on who issued the credit card). The credit card company pays them and then distributes the receivables to all the banks that issue the credit cards.

The bank pays the credit card company and then the bank that issues my credit card sends me a bill and then I pay the bill.

You have the customer, the retailer, the merchant acquirer, the credit card company and the issuing bank involved in just one transaction of buying a candy bar.

With central bank digital currency, the Fed would take it right out of your Fed account and bypass the merchant acquirer, the banks and the credit card company. The process would be streamlined and simplified.

Source: Digital Asset

But This Is What They Don’t Tell You

If the government knows exactly what you’re buying, to whom you’re making donations and (by extension) what you’re reading based on which books you buy, etc., then we have come very far down the road toward thought control, censorship and selective law enforcement against political enemies.

It’s a government that looks like the state ruled by Big Brother in George Orwell’s Nineteen Eighty-Four.

The government will tell you it’s cheaper, faster and safer, and that’s true, as far as it goes. But there are a lot of hidden agendas they are not telling you.

There are a lot of things that are really going on that are important for investors and ordinary citizens to know if you're going to be living in a country that does this.

The Elimination of Cash

The first part of the hidden agenda is to eliminate cash. If you're the government and you want the central bank digital currency to succeed, you have to eliminate cash because it's your competition.

The government has wanted to eliminate cash for a long time. They haven't been able to because people still use it, to some extent. But 90% of our transactions are, in fact, digital.

We do pay with credit cards. Many people get paid digitally. People are wiring you the money. You're paying other people digitally, you're paying your bills online, you're checking your bank account online, doing transfers. That's all 100% digital, even if it's not at the central bank digital currency stage.

So we don't use cash that much, but we have the CHOICE to use it. It is an option and some people have a preference for it. You always want a little cash in your wallet. But the government hates cash because it's not traceable. If you spend it, they don't know that you spend it. They can't put you under surveillance with cash. There are marked dollar bills, but those are reserved for serious criminals.

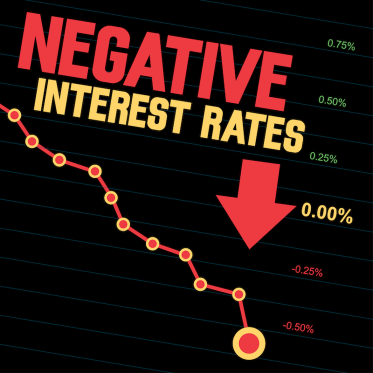

Negative Interest Rates

The other thing the government wants to do is have negative interest rates. I’m not saying we’re going to have negative interest rates anytime soon, but some countries have had them, including Japan and Switzerland.

A negative interest rate works this way: Say you put $100,000 in the bank… Right now, with a positive interest rate, if you put $100,000 in the bank and make 1% on your money, you come back a year later and have $101,000 because they gave you interest.

A negative interest rate is the opposite. Let’s say the negative interest rate was -1%. You put $100,000 in the bank, you go away for a year, you come back, you have $99,000. They took $1,000 away.

You’ll say, “Well, I’m not going to stand for that. I’ll just take all my money out and get cash and put it in a metal container and bury it in the backyard,” or some equivalent of that. The government knows that people would do that. And it was done in the Great Depression for other reasons, though it had to do with people not trusting banks.

So you really can’t have negative interest rates, at least at the consumer level, as long as you have cash because cash doesn’t have a negative interest rate.

You have $100,000, you go away for a year, you still have $100,000. You might not make any money, but at least the government can’t take it away. Going 100% digital grows the threat of negative interest rates simply because the banks are in total control of your money.

Account Freezes

The government wants to use the banking system for a lot of other things. They might want to freeze your account, they might want to seize your assets, they might want to put an expiration date on your money. Imagine you get paid and the government says, “OK, you got the money. Nice job, but that money is going to evaporate or disappear if you don’t spend it in the next six months.” How’s that for a stimulus program?

None of these things is possible if there’s cash around. But if you get rid of cash and force everyone into a digital system, then you can do these kinds of things.

Fiscal Policy

Let me expand on what I just said for a moment. I’ll show you how fiscal policy can be dictated by Biden Bucks. With total control of your money, the government can conduct fiscal policy at will.

What if the government wanted to stimulate the economy and increase the amount of consumer spending? They could simply send you a letter that states, for example, “You must spend $200 in the next 30 days or we will take $100 out of your account as a penalty.” As most citizens will not want to risk losing $100, they will spend the amount requested and create stimulus in the economy as the government had wanted.

This could also work in the opposite direction. Say the government wanted to cool down the economy and not have as much money in circulation. They could encourage savings by requesting a certain balance in your account be kept and not spent. If you went under that set balance, a penalty would be triggered.

The Total Surveillance State

This is the culmination of the total surveillance state. We’re already pretty much under surveillance 24/7, whether you realize it or not.

If you have a mobile phone and have the GPS turned on, you know where you are and where you’re going. But so does the government. They can use your cellphone to track you and that has been done. It is done all the time in criminal investigations and counterterrorism and elsewhere, but it can be done for any political reason at any time.

So what’s the solution to that? Well, some people say to turn off your cellphone. But there’s a battery in it. It still sends out a signal.

Also, the government can track the E-ZPass on your car or use license plate scanners or facial recognition software, or have closed-circuit TV just about everywhere you go. They even have what’s called gait recognition software where they can tell who you are by the way you walk.

So we’re already pretty much under surveillance. Biden Bucks is the last step in the total surveillance state. This is why China did it. And don’t believe anyone who tells you that the United States won’t do it.

The United States is moving closer and closer to a dictatorial-style government. And it’s being enhanced by central bank digital currencies. It’s one more data flow, it’s one more information flow and they can tag you at the physical point of purchase or the online point of purchase, if you’re using a website.

This is done by what you’re buying, who you’re giving money to, what you’re spending money on, where you’re going, etc., all of which are enhanced by central bank digital currencies.

Whether it’s political attacks, the IRS, a new withholding tax, negative interest rates or they just don’t like you, we’re getting more and more to be a country where that’s enough to be in trouble and will be facilitated with the central bank digital currency.

Coming Faster Than Expected

One objection I’ve heard to these warnings about government control is, “Oh, that will never happen here.”

Sorry to tell you this, but it’s happening now.

- Since 2013, there have been several collaborative initiatives between the Federal Reserve and industry stakeholders on strategies for improving the speed, safety and efficiency of the nation’s payment system.

- 2015 — the Federal Reserve convened the Faster Payments Task Force (FPTF), a 320-member group comprised of a broad range of industry participants, to identify and assess alternative approaches for implementing instant payment capabilities in the United States.

- 2018 — the Fed facilitated the industry’s Faster Payments Governance Framework Formation Team, which concluded its work and launched the U.S. Faster Payments Council, an industry-led membership organization that is intended to develop collaborative approaches to accelerate U.S. adoption of payments.

- 2022 — the Fed, in cooperation with giant global banks, launched a 12-week pilot project to test the message systems and payment processes on the new CBDC digital dollar.

A pilot project is not research and development. That’s already done. The pilot means Biden Bucks are here, and the backers just want to test the plumbing before they roll the system out on the entire population. - 2023 — U.S. Under Secretary of Treasury Nellie Liang said in a speech:

“Leaders from Treasury, the Federal Reserve, and White House offices, including the Council of Economic Advisers, National Economic Council, National Security Council and Office of Science and Technology Policy, will begin to meet regularly to discuss a possible CDBC and other payments innovations. To support these discussions, the CBDC Working Group is developing an initial set of findings and recommendations.”

And then… - March 15, 2023, the Fed announced the launch of its FedNow Service. Its press release is here. The FedNow Service will process and settle individual payments within seconds, 24 hours a day, seven days a week, 365 days a year. Like other payment and settlement services offered by the Federal Reserve, the service will settle obligations between depository institutions through debit and credit entries to balances in their master accounts at the Reserve banks.

- July 1, 2023 — the official launch of the FedNow service… a testing of the waters for full CBDC implementation

What do all these developments mean?

They mean the government has been, step by step, heading toward implementing CBDCs into the U.S. payment system.

Once the CBDC is rolled out, the government will order citizens to hand in their physical paper cash, which will be burned in incinerators. At that point, the pigs (all of us) will be in the slaughterhouse ready for the digital slaughter of negative interest rates, account freezes, tax withholding and outright confiscation for those with the wrong political views.

Implementation Is Happening Globally

In a world of CBDCs, the government will know every purchase you make, every transaction you conduct and even your physical whereabouts at the point of purchase.

It’s a short step from there to negative interest rates, account freezes, tax withholding from your account and even putting you under FBI investigation if you vote for the wrong candidate or give donations to the wrong political party.

If that sounds like a stretch, it’s not.

Different countries are at different stages of implementing it. We call the dollar version of this Biden Bucks, but the concept has been around for a while. Biden has just accelerated the rollout of this in the United States in particular.

If you had asked me about this two years ago, I would have said the U.S. is taking a much more studious approach to it. It was too important to not be involved in, but the U.S. did not seem to be in any hurry to actually implement it.

There were studies, and I would have said my estimate at the time would have been, “OK, China has it. Europe, maybe another year. The U.S. might be three or four years down the road because the dollar’s too important. They don’t want to race into it. They want to get it right. There are a lot of ways to mess it up.”

But that’s changed under Joe Biden.

Biden has now fast-tracked this thing. We’ve moved pretty quickly from what I would call a research phase to an implementation phase. So we give it the name Biden Bucks, because Joe Biden will prove to have been responsible for actually implementing this at a very quick tempo in the United States.

Numerous Western nations, including England and Canada, along with the central banks of Uruguay, Thailand, Venezuela and Singapore are also exploring CBDCs.

There are already some examples of government action targeting citizens under the guise of CBDCs…

China

The kind of surveillance I have mentioned is the real driving force behind the Chinese CBDC.

China already uses facial-recognition software, mobile phone GPS tracking and the purchase of plane or train tickets to track their citizens. This surveillance can be used to detect anti-state activities and to arrest dissidents or anyone who does not strictly follow the orders of Chairman Xi.

China’s lead in the race to produce the first major central bank digital currency is well-known. The Chinese CBDC is already being used in prototype form and was introduced at the 2022 Winter Olympics in Beijing.

But China has revealed an even greater ambition. It wants to take its rules for the use of CBDCs and make them the global standard. It’s likely that many Asian and African countries might agree in exchange for assistance from China.

Once China’s totalitarian surveillance software is perfected, they can make it the standard for other countries and facilitate intrusive 24/7 surveillance by every dictator and autocratic leader in the world.

No doubt China would arrange to have access to the same surveillance information it was providing to client states. This is what’s coming to the U.S. when Biden Bucks are implemented.

Nigeria

In 2022, the Central Bank of Nigeria announced a cap on customer ATM withdrawals in a bid to promote usage of its digital currency called eNaira.

The banking regulator said the maximum customer ATM withdrawal for naira was capped at the equivalent of $45 per day, compared with earlier daily limits of the equivalent of $337 per day.

This move was to reduce the use of cash and promote digital currencies to “increase access to banking services.”

After a public uproar, the central bank raised the level to the equivalent of $1,120 weekly.

Canada

In 2022, Canadian truckers staged a protest against COVID vaccine mandates by creating a Freedom Convoy, which staged a blockade in Ottawa. The government arrested the truckers and held them without bail. They also froze their bank accounts.

The Trudeau government used digital bank accounts as a weapon against political opponents. It’s not hard to realize the same thing can be done in the U.S. and even easier with Biden Bucks.

What happens when there is no physical cash and your bank account is frozen? With Biden Bucks, the government will be able to force you to comply with its agenda. Because if you don’t, they could turn off access to your money.

Trillions in Wealth Could Be Wiped Out

Do you remember the sequence of players involved in the example of buying one candy bar mentioned earlier?

Major banks fear they will be completely disintermediated in the payments system. Individuals will have their own personal accounts at the Fed from which they can pay or receive funds with the wave of a smartphone.

Who needs bank accounts, checks, account statements, deposit slips and the other clunky features of a banking relationship when you can go completely digital with the Fed?

Mastercard and Visa are also concerned that their payment channels will be made redundant. An individual Fed account on your mobile phone could eliminate the 2.5% fees that merchant acquirers charge retailers to process your credit card transactions.

That’s why investors need to take these developments seriously. There’s more at stake than just customer convenience. Trillions of dollars of wealth in the form of financial institution stock prices of companies such as JPMorgan, Citi, Mastercard and Visa could be wiped out as the new digital payment technology takes hold.

Remember this… Railroads were one of the largest sectors of the economy from 1870–1930, but were mostly bankrupt by the 1970s. General Motors has been rescued from bankruptcy more than once by the U.S. government. General Electric was once an industrial giant and now it is a shell of what it once was. Oil company stock prices have taken a beating from the threats of the Green New Deal.

Things change. Banks and other financial institutions dominate stock market valuations today alongside the tech sector. Now CBDCs are coming for the banks. Investors should watch developments closely and be nimble when it comes to getting out of financial stocks before the digital dollar eats their lunch.

Access to Your Money Is Under Siege

When news hit that Silicon Valley Bank and Signature Bank (both ranked in the Top 30 in bank assets in the U.S.) collapsed, it caused depositors across the country to worry if their money is safe in any bank. Maybe you are one of them.

When depositors worry about a bank’s ability to make good on its deposits, it can quickly become rational to panic, move deposits out and ask questions later.

That’s the essence of a bank run.

Whether an account is in CBDC (Biden Bucks) or a regular checking account doesn’t make that much difference. Bank runs today are no different than in the 1930s from a behavioral perspective.

It’s all about lost confidence, fear, not wanting to be the last person out of a burning building, rumors, word of mouth and a host of psychological factors that are part of human nature.

That part hasn’t changed since at least the 14th century with the failures of the Bardi and Peruzzi banks around 1345. See here.

What has changed is technology. Marshall McLuhan said in the 1960s that in the global village, everyone knows everything at the same time. He was right. That means when a bank run begins, there’s an immediate reaction.

The difference with the 1930s is that you don’t typically line up around the corner and wait for the chance to demand cash from the teller. You take out your cellphone, make a few taps and, whether it’s Venmo or a wire transfer, the money is on its way out the door.

Whether it’s CBDC, Venmo, wire transfer or cash from an ATM, everyone is cashing out at the same time via digital channels. The only exception to this are insiders who can see the meltdown before the public. They tend to get all their money out.

But there is one huge impact of CBDCs that’s entirely new and sets them apart from what’s described above. CBDCs are programmable and controlled by the government. This means when a run develops, the government can stop the run just by freezing CBDC account transfers.

They can even claw back earlier transfers.

Since the government controls the CBDC ledger, they can see where the early withdrawals went and simply reinstate them on the account of the failing bank and debit them from the accounts of the transferees. The government can do this with a few keystrokes because they see everything.

This means that once Biden Bucks are implemented, you’re locked into a system controlled by the government. You’re in a money jail. There’s no point even starting a bank run because the government can track your movements and put the money back where it started.

It’s one of many ways that Biden Bucks give the government total control of your money and the ability to monitor your thoughts and movements.

Your Next Steps

You might not be able to fight back easily in the world of Biden Bucks, but it can be done.

There is one nondigital, nonhackable, nontraceable form of money you can still use…

Gold

Gold has proven the ultimate calamity-proof investment through the centuries. It never loses its fungible quality. It never loses its luster. And it never loses its universal appeal as “real” money. Gold and silver may not be a medium of exchange today, but they will quickly regain that status as Biden Bucks are implemented.

The question is what is the best form of gold and silver for use in feeding your family or buying necessities?

Bars are fine for wealth preservation, but they are not practical for payments. Bars are either 1-kilo or larger (400 troy ounces for a Good Delivery gold bar), so the value is too high for day-to-day transactions. Small bars of 10 grams or so are available, but they are unfamiliar to most people and the metric system denominations might require some explanation.

I recommend coins from the U.S. Mint. The U.S. Mint is a guarantee of quality that might not exist if you’re using private mint or commemorative coins.

The two main types of bullion coins are American Silver Eagles and American Gold Eagles. The Silver Eagle is pure silver and weighs 1 troy ounce. It’s basically a purer version of the old silver dollar some of us remember from when we were kids, except it’s worth $25.00 today.

How do you get started buying physical gold?

I recommend you get yours from our friends at Hard Assets Alliance.

Hard Assets Alliance allows you to buy and take delivery of physical gold (and other precious metals) at exceptionally low costs.

You can also buy and store your metal in your choice of five audited vaults worldwide.

It’s the hands-down easiest way to get started with gold, silver and other metals.

It’s FREE to sign up for an account. Once you’ve completed the short account-opening process, you’ll be able to shop for the metals you want to buy right away.

It’s a great private online experience.

Goldbacks

Goldbacks are a form of gold not affected by inflation and can provide an alternative to the U.S. dollar as a form of payment and store of wealth.

They are thinly printed sheets of real gold that have been covered in a nearly indestructible protective polymer and look and feel almost like real cash.

Goldbacks are crafted with .999 fine gold paint on Aurum and have a plastic film designed to hold in the gold paint, ensuring its durability. Printed on clear polyester in a four-color process, the Aurum covering adds an extra level of protection so that the gold foil notes can be easily held, admired and utilized as currency

“Off the Grid” Assets

Jewelry has many advantages during periods of asset seizures, chaos and civil unrest.

Here’s why.

The government can outlaw the ownership of gold bullion and has. But it has never outlawed owning gold in all forms… just bullion. Citizens merely owned the gold in jewelry form. If the government controls your bank account, owning gold jewelry is a way to still own assets that contribute to your wealth.

Land and fine art are also hard assets to own as the government switches to digitize your physical cash. These are assets that will last and are out of the reach of digital manipulation.

Conclusion

In the United States of America, many aspects of our lives are already under surveillance. Biden Bucks are the last step in the total surveillance state and total control of your money.

Don’t believe the government when they tell you this is just an easier and faster way to make payments.

This is another step toward government control, both of your money and your individual right to privacy.

The U.S. is moving closer and closer to a dictatorial-style government. And it’s being enhanced by central bank digital currencies luring us into a financial mousetrap.

With Biden Bucks, the government would become both money printer and bank, destroying any checks and balances to their power over Americans’ financial holdings.

But we can fight back by adopting a variety of alternative currencies including cash (while it lasts), gold coins, silver coins, cryptocurrencies and commodity barter.

That’s one reason the government is trying to eliminate cash and kill crypto. It may come down to gold and silver. Get yours while you still can.

The government is coming after our money and rights… it’s up to us to preserve our freedoms as Americans and fight back.